| All content presented here and elsewhere is solely intended for informational purposes only. The reader is required to seek professional counsel before beginning any legal or financial endeavor. |

Whether it's tax season, or you just need a snapshot of your restaurant's financial performance, the restaurant's income statement is the financial statement you’ll be turning to. A great amount of effort and attention can be needed to generate these statements, but if you’re aware of what goes into creating a restaurant income statement, and what it may be used for, chances are you’ll be a step ahead of the rest in having the right document at the right time.

What Is an Income Statement?

A restaurant income statement is a financial statement, typically prepared by owners or bookkeepers that show the restaurant's income and expenses over a given period of time. A restaurant's income statement is no different than any other business's income statement in terms of information presented, but there can be some line items unique to the business.

It is also known as a profit and loss statement, or income expense statement, which shows the profitability of the business over a period of time. Most common examples you may hear are “Annual Profit Loss” statements, which may refer to January 1 through December 31 income and expenses.

What Information Is Included in a Restaurant Income Statement?

There are many sections of a restaurant's income statement. Below we outline some of the common items and what a restaurant statement may look like given the nature of the business.

Section One: Sales - The sales portion will show the gross amounts paid to you by customers. A restaurant may have items like food, beverages, alcohol, and potentially revenue from catering events or to go orders.

Section Two: Cost of Goods Sold - The cost of goods sold is the direct costs the restaurant has paid to generate the sales. Think of this as the cost you paid for the items sold. For restaurants this may look like the cost of the food purchased, alcohol purchased, and possibly packaging that went into the final product which was sold.

Section Three: Labor Costs - Labor is the human power used to create the item sold plus any administrative or waiting staff. The wages paid to the people of your business go into this section, which is commonly referred to as “wages” or “payroll”

Section Four: Operating Costs - Operating costs are the other costs associated with your business, such as utilities, subscriptions to softwares, professional fees, licenses, taxes, and so on; these costs may not be directly correlated to cooking and selling foods, but necessary to keep the lights on.

Section Five: Net Profit or Loss - Your sales minus all your expenses (sections two through four) will generate either a net income amount (positive) or net loss amount (negative). Ideally you would want to come out positive, but that may not always be the case; however you now have a tool which will show you line by line where the money generated is going.

What Is a Restaurant Income Statement Used for?

A restaurant income statement is a common tool utilized for filing taxes, checking financial performance, applying for financing, and many more. Having this document handy gives you the information source to show to any person or entity interested in how your restaurant is operating over a period of time.

How Do You Calculate Restaurant Income?

To calculate your restaurant's income you can use the below formula. It leverages the five sections explored above, but in essence totals the money coming into the business, and subtracts the costs the business paid over the same period of time. The equation is as follows:

Net profit/loss = total sales - COGS - labor cost - operating cost

How to Prepare a Restaurant Income Statement

There are many ways to complete a restaurant income statement, from using a professional or accounting software or completing manually, they follow the same general steps

Step 1: Select a period of time for reporting - You will need to begin by defining a period of time you’d like your financials to cover. Typically owners think in terms of annual, quarterly, and monthly. The period of time will set the parameters for which you’re measuring revenues and costs.

Step 2: Compile all your transactions - The next step is one of the most important; you’ll need to gather all the revenues and costs for the period you’re looking to measure. This means all sales reports, bank statements, and any cash transactions.

Step 3: Categorize these transactions - At this point you’ll see why utilizing an accounting software for completing your restaurant income statement is a great idea; in this step you will need to categorize the transactions into either revenue, cost of goods sold, labor, or operating costs. Doing this will allow you to complete the steps to reach your net income or loss.

Step 4: Total your amounts - Now that you have all the transactions categorized the next step will be to total the amounts into single groups, for example, if you have 104 lines of sales transactions all marked as “revenue”, you will total these to have one line called “Revenue” showing the total of those 104 lines. Repeat this for each group of transactions.

Step 5: Calculate your net income or loss - At this point you should be looking at your totals for each category for the period of time you set out to measure. This is where we apply the calculation for net income or loss; Net profit/loss = total sales - COGS - labor cost - operating cost. This is the final step to completing your restaurant's income statement.

Should I Prepare an Income Statement Myself or Hire a Finance Professional?

Depending on your familiarity with the process, how many transactions you are looking to measure, and what tools you are using, the answer to whether you want to hire a professional is that it depends.

Typically it is advised to use an accountant or bookkeeper if you are less familiar with the process, relying heavily on the information output, or the nature of your business is not as straightforward as only sales and costs (for example utilizing restaurant business loans, or business to business transactions).

How to Analyze Your Restaurant Income Statement

A great rule of thumb to follow when analyzing restaurant income statements is the 30/30/20/20 rule, which we’ll outline below. There are many ways to read a financial statement and owners typically develop this skill over time.

Metrics to Track in Your Restaurant Income Statement

Typically the basic measure of an income statement is understanding the sections of the financial statements weight in proportion to your total revenue. This means taking for example a cost and dividing it by your revenue to determine the percentage.

- Sales - Sales can be looked at over periods of similar time. If you are looking at a quarterly income statement, are your sales higher or lower than the previous quarter? What about the same quarter from the previous year? This will gauge how growth is going.

- Cost of Goods Sold (COGS) - Owners typically like to apply the 30/30/20/20 rule to the cost of goods sold. This rule states your COGS should be 30% of your total revenue. This may look like COGS being $30,000.00 and your revenue $100,00.00 ($30,000.00/$100,000.00). The rule applies also to labor (20%), and operating costs (30%), with the final 20% being your net income.

- Gross Profit and Gross Profit Margin - Gross margin differs from gross profit. Gross profit is just your revenue less COGS, this is a dollar amount. In our previous example you would find:

$100,000.00 revenue - $30,000.00 COGS = $70,000.00 gross profit

Gross margin looks to create a percentage from this figure by taking your gross profit and diving it be revenue, or in our example:

$70,000.00 gross profit / $100,000.00 revenue = 70% gross margin

Net Profit/Loss - Similar to sales, this is a metric to measure over similar periods of time or as a trend. Your goal may be continuous growth or to turn a profit. Measuring this metric over time you can see how your business decisions have translated to financial results.

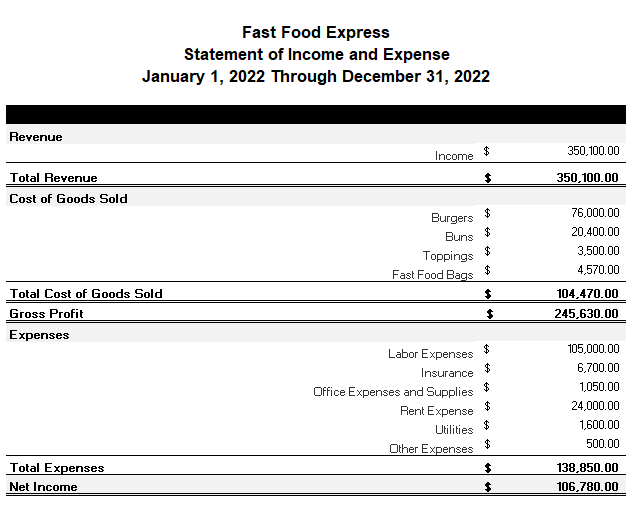

Example of a Restaurant Income Statement

While there is no standard format to follow in terms of presentation we summarize all the learnings above in the below an example of what you might expect to see:

Final Word

Restaurant income statements are a powerful tool owners can use to measure their business decisions and determine how those decisions translate to financial impact. While they may not be the simplest statement to prepare, having one handy is crucial for owners to understand where the business stands and not allow for any opportunities to pass.